Should US Citizens in Canada Set Up a Corporation?

Summary

If you are a U.S. citizen living in Canada and thinking about incorporating your business, you need to pause.

Without proper cross border planning, you could face extremely high tax rates. In some cases, over 80 percent.

There are three main scenarios:

-

No planning. The U.S. taxes you immediately under ‘net CFC tested income’ (formerly known as GILTI) rules.

-

High tax exception election. This can help, but it does not always apply.

-

Section 962 election. Often, this is the most practical solution.

Let us walk through this in simple language.

Important Assumption for This Article

- All numbers assume Ontario’s highest general corporate tax rate of 27 percent

- In reality, most Canadian resident business owners are eligible for the small business deduction on their first $500,000 of active business income. That can reduce corporate tax to around 12 percent in Ontario.

- We are ignoring that lower rate in the base example to simplify the illustration.

- Ironically, the small business deduction can actually create more U.S. tax problems. We will explain why shortly.

- Also, we assume dividends from the corporation are paid in a different year where the corporation is not earning income.

- If dividends are paid in the same year as the corporate earnings, this can mitigate some of the double tax by way using some of foreign tax credit from the dividend against the corporate earnings.

Why This Is Complicated

Canada taxes corporations and then taxes dividends when you take money out.

The U.S. taxes its citizens no matter where they live. If you own a Canadian corporation, the IRS may treat it as a controlled foreign corporation (CFC).

That means the U.S. may tax you on corporate profits even if you never take the money out.

Scenario 1: No Planning

The Expensive Surprise

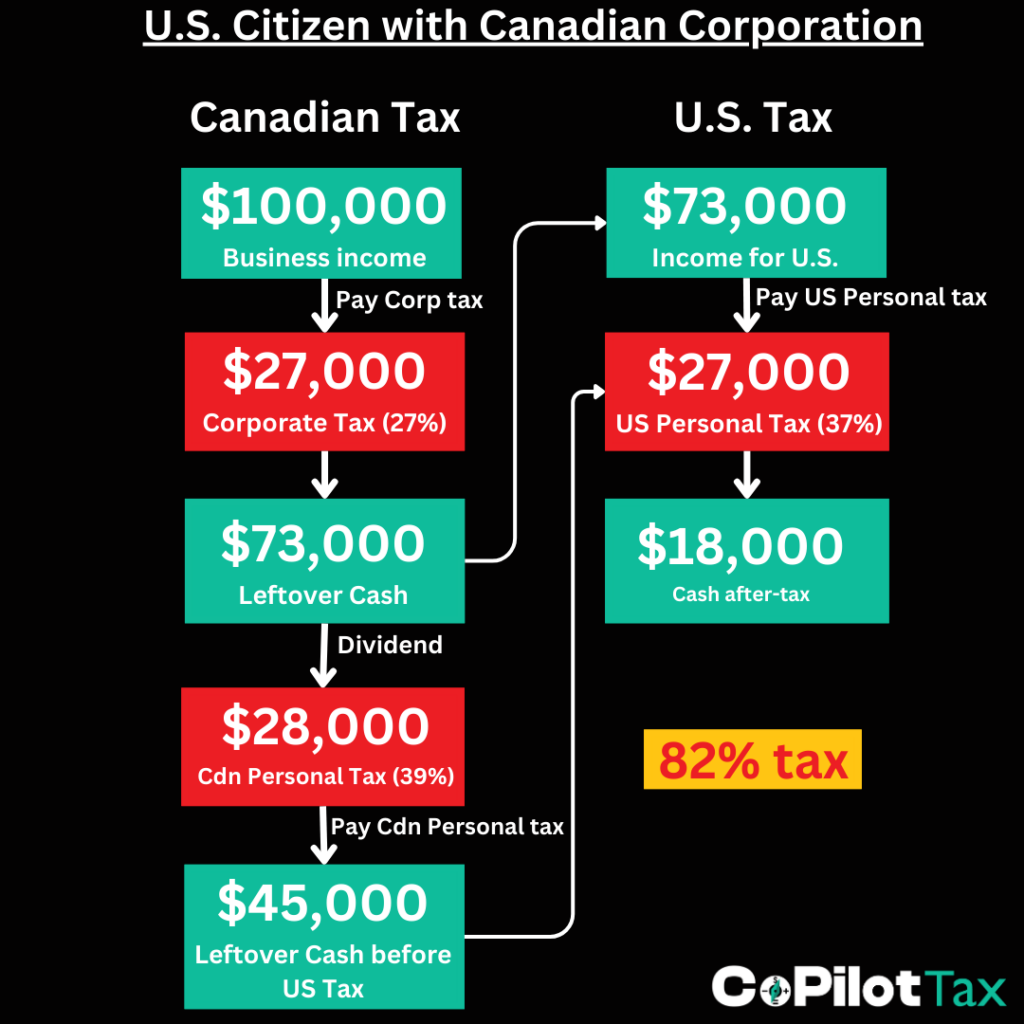

Assume your Canadian corporation earns $100,000.

Step 1: Canadian Corporate Tax

Business income: $100,000

Corporate tax at 27 percent: $27,000

Cash left in the company: $73,000

So far, normal Canadian planning.

Step 2: U.S. Tax Under Net CFC Tested Income

Here is the shock.

The U.S. does not care that you already paid Canadian corporate tax.

Under the net CFC tested income rules, the IRS will tax you personally on certain corporate profits.

There is generally no direct foreign tax credit available at this stage for the Canadian corporate tax you already paid.

So the U.S. may say:

“You have $73,000 of income. Pay U.S. personal tax on it.”

Assume a 37 percent U.S. rate.

U.S. tax: about $27,000

You have now paid:

-

$27,000 Canadian corporate tax

-

$27,000 U.S. personal tax

And you have not even taken the money out yet.

Note that this is a simplified example and capital assets and other adjustments can change the calculation.

Step 3: Canadian Personal Tax on Dividend

When you eventually pay yourself a dividend:

Canadian personal tax at 39 percent: about $28,000

You started with $100,000.

You could end up with roughly $18,000 in your pocket.

The U.S. won’t tax you again since they already taxed you but that s about 82 percent total tax.

This is why incorporating without U.S. advice can be dangerous.

Scenario 2: High Tax Exception Election

A Partial Solution

The U.S. has a rule that says:

If your foreign corporation pays a “high enough” corporate tax rate, the IRS will not tax you immediately.

The threshold is roughly 19 percent.

In our example, Ontario’s 27 percent general corporate rate exceeds that.

So in this situation:

-

Canadian corporate tax: $27,000

-

No immediate U.S. tax

You only deal with U.S. tax later when dividends are paid.

That is much better than Scenario 1.

The Problem With the Small Business Deduction

Now here is the twist.

If you qualify for the small business deduction, your corporate tax rate may drop to around 12 percent or less.

That is below the 19 percent threshold.

If that happens:

You may not qualify for the high tax exception.

And you are back to Scenario 1.

So the very thing that saves you Canadian tax may trigger more U.S. tax.

Scenario 3: Section 962 Election

Often the Most Practical Option

The Section 962 election allows a U.S. citizen to be taxed similarly to a U.S. corporation on certain foreign corporate income.

In simple terms:

-

Instead of paying U.S. personal tax at up to 37 percent

-

You pay U.S. corporate tax at 21 percent. But, this can be reduced. You get a 40% deduction AND you can use your Canadian corporate tax to offset the U.S. tax.

Step 1: Canadian Corporate Tax

Business income: $100,000

Corporate tax at 27 percent: $27,000

Cash left: $73,000

Step 2: U.S. Corporate Style Tax at 21 Percent

Under Section 962:

You get a 40% deduction so the income is $60,000 instead of $100,000.

The U.S. calculates tax at 21 percent.

21 percent of $60,000 = $12,600.

Now the key benefit:

You can generally claim a foreign tax credit for Canadian corporate tax paid.

Since Canadian corporate tax was $27,000 and U.S. corporate tax is $12,600:

Even though you won’t get the full credit of the foreign tax credit due to limitations (only 90%), the foreign tax credit can reduce the U.S. corporate level tax to zero.

So the first layer of U.S. tax may be eliminated.

Step 3: When Dividends Are Paid

When you take money out:

You may still owe some U.S. personal tax.

Often this ends up being around 3 percent to 4 percent due to technical rules such as net investment income tax.

In our example:

Final after tax cash: about $42,000

Effective tax rate: about 58 percent.

Is it perfect? No.

Is it dramatically better than 82 percent? Yes. And nearly identical to what a Canadian in Ontario would pay (roughly 55%).

Key Takeaways

If you are a U.S. citizen in Canada:

-

Incorporating can be very expensive unless you get proper cross border advice to mitigate the U.S. impact.

-

Without planning, the U.S. may tax you again even if you already paid Canadian corporate tax.

-

There are two main ways to mitigate this:

-

High tax exception election

-

Section 962 election

-

-

Section 962 is often the most practical solution.

-

Filing requirements become much more complex. Forms like Form 5471 carry penalties starting at $10,000 per year per form.

Final Thought

In Canada, incorporation is often a smart strategy.

For U.S. citizens, it can create unexpected double taxation unless it is structured properly.

Before incorporating or continuing with your current structure, it is worth reviewing:

-

Your corporate tax rate

-

Whether you qualify for the high tax exception

-

Whether a Section 962 election makes sense

The difference can be tens of thousands of dollars per year.

If you are a U.S. citizen operating a Canadian corporation and are unsure whether your structure is optimized, now is the time to review it.

Book a consultation and make sure your corporation is working for you, not against you.