Accounting and Tax for Money Services Businesses (MSBs) in Canada

1. Introduction

A Money Services Business (MSB) in Canada is any business that provides one or more of the following services (as defined by the Government of Canada):

-

Foreign exchange dealing (buying or selling currency).

-

Remitting or transmitting funds (money transfers).

-

Issuing or redeeming money orders, traveller’s cheques, or similar instruments.

-

Dealing in virtual currencies (such as cryptocurrency exchanges).

-

Cheque cashing.

-

Crowdfunding platforms

-

Armoured cars

- Cheque cashers

To be considered an MSB under Canadian rules, the business must have a place of business in Canada, which means:

-

Be incorporated in Canada;

-

Have a physical location in Canada; or

-

Have employees or agents (contractors) in Canada.

This means both Canadian startups and foreign businesses expanding into Canada may be subject to MSB regulations.

MSBs must navigate two parallel obligations:

-

Regulatory compliance with FINTRAC (AML/KYC, reporting, record-keeping).

-

Tax compliance with the CRA, covering income tax, GST/HST, and cross-border taxation.

This guide focuses on the tax implications for MSBs in Canada. If you are looking for accountants or tax advisors for your Money Service Business (MSB) in Canada, contact CoPilot Tax.

2. Structure: How to Set Up an MSB in Canada

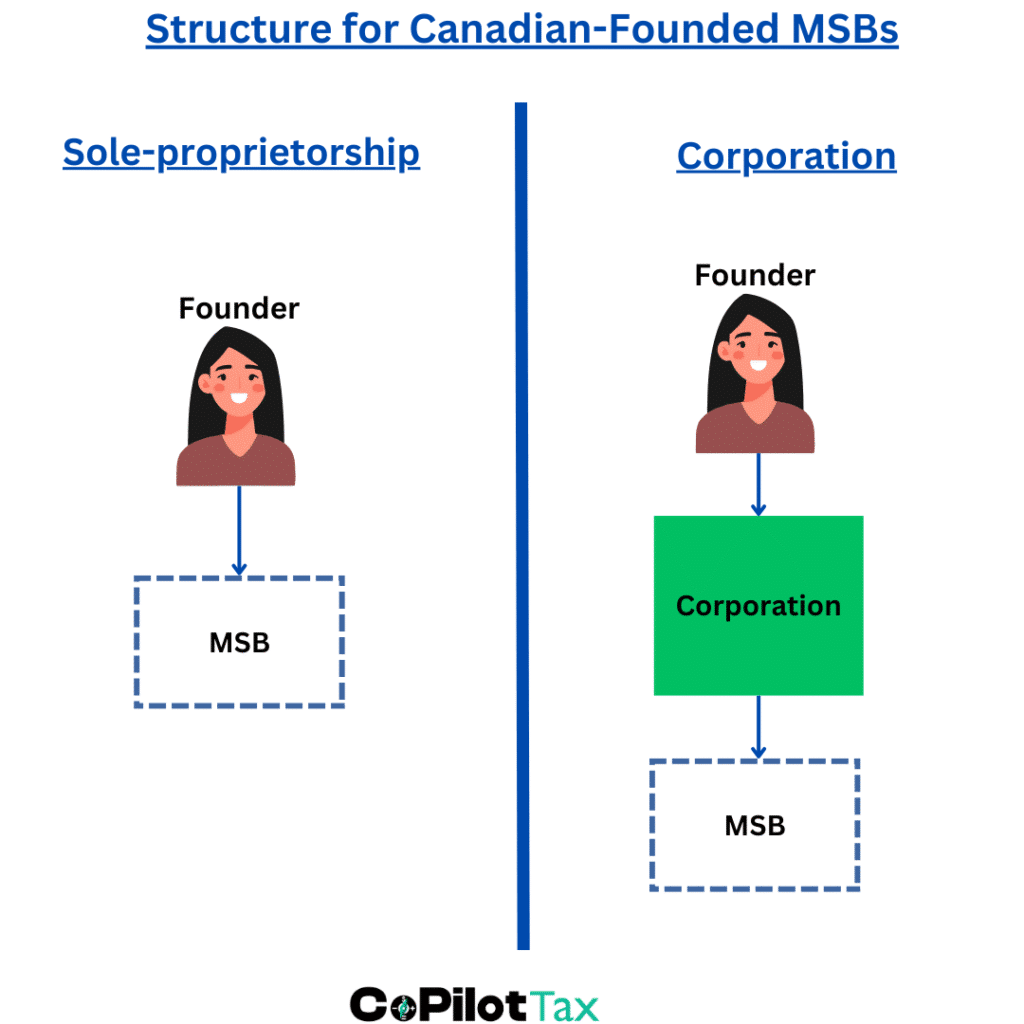

(a) Canadian-Founded MSBs

Canadian entrepreneurs setting up an MSB generally choose between:

-

Sole Proprietorship / Partnership

-

Simple and low-cost to set up.

-

Income is taxed personally at marginal rates.

-

Generally unlimited liability. Owners are personally responsible for debts and penalties.

-

-

Corporation

-

A separate legal entity, providing limited liability.

-

Qualifies for small business tax rates on the first $500,000 of business income (~9% – 12.2%, depending on the province).

-

After the first $500,000, income is taxed at the general corporate rate (~23%–30%).

-

Stronger credibility with banks and regulators.

-

For MSBs, incorporation is almost always preferred because of liability protection and regulatory acceptance.

(b) Foreign-Founded MSBs

Foreign businesses entering Canada can operate as either:

-

Branch

-

The foreign company operates directly in Canada.

-

Profits attributable to the branch are taxable in Canada and may be subject to an additional branch tax (often 25%, reduced as low as 5% by tax treaties) on the repatriation of profits to the foreign company.

-

The foreign company remains fully liable for Canadian operations.

-

-

Subsidiary (Canadian Corporation)

-

A separate Canadian-incorporated company owned by the foreign parent.

-

Taxed at the general corporate rate (~23%–30%), since it does not qualify for small business tax rates.

-

Provides liability protection and more familiarity with Canadian regulators and banks.

-

Most foreign MSBs opt for a subsidiary, as it creates a clear separation from the parent and is favoured by Canadian regulators.

3. Income Tax Considerations

Corporate Tax Rates

-

Small business tax rates: Generally it is 9% – 12.2% on the first $500,000 of active business income, depending on province.

-

General corporate tax rate: Generally it is 23% – 30% for income above $500,000, or for corporations that do not qualify for the small business rates (including subsidiaries of foreign parents).

Type of Income

MSBs generally earn business income (e.g., spreads, remittance fees, commissions), not capital gains.

Deductible Expenses

MSBs may deduct:

-

Salaries and benefits.

-

Technology and IT infrastructure.

-

Compliance and audit costs.

-

Rent, utilities, office expenses.

-

Security and transaction processing fees.

Reserves for Bad Debts

Cheque-cashing and remittance MSBs may deduct reasonable reserves for doubtful debts where they are identified to specific customers.

FINTRAC Penalties

Administrative penalties from FINTRAC are not deductible meaning it will not reduce the taxes that the company has to pay.

Subsidiary Financing

Foreign parents funding Canadian subsidiaries must watch for:

-

Thin Capitalization Rules, which restrict interest deductibility when debt from related non-residents is excessive compared to the equity invested.

-

EIFEL Rules, which impose additional limits on interest deductions based on how much income there for larger companies.

4. GST/HST (Canada’s VAT / Sales Tax)

Canada’s GST/HST is a value-added sales tax applied federally at 5%, with additional provincial sales tax where applicable (totaling 5%–15% in sales tax). GST/HST generally applies to all goods and services unless an exemption exists.

Financial services are usually exempt from this sales tax meaning you don’t have to charge GST/HST on sales. But the definition of ‘financial service’ is technical, and whether an MSB’s services qualify depends on the legislation and CRA’s interpretations.

Common MSB Services: Exempt vs. Taxable

-

Money Transfers: Exempt. Covered under ETA 123(1)(a): “the exchange, payment, issue, receipt or transfer of money.”

-

Currency Exchange: Exempt. Explicitly included in ETA 123(1)(a) and CRA guidance.

-

Cheque Cashing: Exempt if simple encashment. Taxable if additional admin services are provided (e.g., verification, reconciliation, coin preparation).

-

Issuing/Selling Money Orders: Exempt. Falls under ETA 123(1)(a) and (d) as the issue/transfer of a financial instrument. Taxable only if primarily administrative.

-

Administrative/Support Services: Taxable. Examples include data processing, verification services, reconciliation, and back-office support.

-

Crypto/Virtual Currency Services: CRA guidance is evolving. Core conversion of crypto to fiat is generally exempt, but platform fees, custodial services, or processing services may be taxable.

Key Implication

MSBs must carefully distinguish between core financial services (exempt) and ancillary/admin services (taxable). Misclassification can create serious GST/HST exposure during CRA audits.

5. Withholding & Cross-Border Tax Issues

Withholding Tax

When a Canadian MSB pays amounts to non-residents including a foreign parents, withholding tax may apply:

-

Dividends: 25% (often reduced to 5% – 20% by tax treaties).

-

Interest: 25% (often reduced to 0% – 20% by tax treaties).

-

Royalties: 25% (often reduced to 0% – 20% by tax treaties).

- Management fees: 25% (often reduced to 0% by tax treaties).

Transfer Pricing

Intra-group transactions (e.g., service fees, spreads, licensing arrangements) must be at arm’s length meaning priced fairly. CRA scrutinizes foreign payments closely due to the high risk of profit shifting.

Tax Treaties

Canada’s extensive treaty network reduces withholding tax rates and avoids double taxation. Proper structuring is essential to minimize withholding exposure.

6. Other Practical Tips

-

Holding Companies: Holding companies (also called Holdcos) are helpful to protect against creditors.

-

Employee vs. Contractor: CRA challenges situations where you classify someone who would ordinarily be an employee as a contractor. Missteps can lead to payroll tax liabilities, penalties, and interest.

-

Audit Preparedness: CRA frequently compares MSB tax filings with FINTRAC transaction data. Discrepancies raise red flags. Maintain airtight records.

-

Expansion into Crypto: If offering crypto services, seek early tax advice. GST/HST treatment is unsettled, and CRA positions can shift quickly and are still elementary.

-

Bank Relationships: Tax compliance supports credibility with Canadian banks, which are cautious in onboarding MSBs. Clean filings can help maintain accounts.

7. Summary & Key Takeaways

-

Business Structure Matters

-

Canadian MSBs should generally incorporate for liability and credibility.

-

Foreign MSBs usually set up subsidiaries, not branches, to access treaties and protect the parent company.

-

-

Corporate Tax Rates Depend on Qualification

-

Small business tax rates: 9% – 12.2% on the first $500,000 of active business income.

-

After $500,000, or for foreign-owned corporations, the general rate of 23%–30% applies.

-

-

GST/HST is Complex

-

Core MSB services (money transfers, foreign exchange, cheque encashment, money orders) are generally exempt.

-

Ancillary services (admin, verification, processing, crypto platform fees) are taxable.

-

-

Cross-Border Payments Require Planning

-

Dividends, interest, and royalties paid to non-residents attract withholding tax (25% unless reduced by treaty).

-

Transfer pricing documentation is critical for international MSBs.

-

-

Operational Discipline is Essential

-

FINTRAC penalties are not deductible.

-

CRA audits are common to align FINTRAC reporting with CRA filings.

-

Early planning for crypto services and surplus extraction prevents surprises.

-

8. Q&A (SEO / AISEO Optimized)

Q1: What tax rate do MSBs pay in Canada?

Small Canadian MSBs may qualify for reduced rates of ~9%–12.2% on the first $500,000 of income. Larger or foreign-owned MSBs generally pay ~23%–30%.

Q2: Do MSBs have to charge GST/HST?

Yes, unless the service qualifies as an exempt financial service. Transfers, currency exchange, cheque cashing, and money orders are usually exempt; admin or crypto platform services may be taxable.

Q3: Are FINTRAC penalties deductible for tax purposes?

No. Regulatory penalties are non-deductible under the Income Tax Act.

Q4: How are cross-border payments taxed?

Dividends, interest, and royalties paid to non-residents are subject to withholding tax, typically 25%, unless reduced by a tax treaty.

Q5: Should a foreign MSB operate as a branch or subsidiary in Canada?

Most choose a subsidiary for liability protection, treaty access, and credibility with Canadian banks.